The Colombo Bourse opened strong and climbed sharply during the early session, before easing through the late morning amid profit-taking and selling pressure.

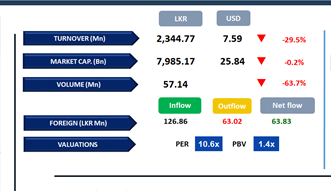

ASPI declined by 37 points to close at 22,293 and the S&P SL20 moved down by 4 points to end at 6,066. Top negative contributors to the ASPI were DOCK, SFCL, RICH, MELS and BREW.

HNW and retail investors’ participation remained subdued, generating a low turnover of LKR 2.3Bn, which is about 38% below the monthly average of LKR 3.8Bn.

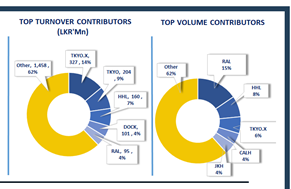

The Materials sector accounted for 27% of total turnover, while the Capital Goods and Diversified Financials sectors contributed a combined 36%. Foreign investors turned net buyers, posting a net inflow of LKR 63.8Mn.

BOND MARKET

A quiet trading session on low participation

The secondary bond market confronted a quiet session with low volumes and limited trading activities. Among the trades that took place, 01.05.2028 maturity traded within the range of 9.00%-9.04% and 15.03.2031 maturity changed hands within the range of 9.85%-9.89%.

On the external front, the LKR slightly depreciated against the USD, closing at LKR 309.65/USD compared to LKR 309.54/USD seen previously.

Overnight liquidity in the banking system contracted to LKR 66.1Mn from LKR 79.9Mn recorded on the previous day.

Meanwhile, Sri Lanka Purchasing Managers’ Index (PMI) for Manufacturing and Services recorded index values of 55.5 and 50.5, respectively, in November 2025.

This indicates a MoM expansion in Manufacturing activities, with favorable contributions from all the sub-indices. Moreover, Services indicated a slower expansion compared to October, partly reflecting the impact of adverse weather conditions, despite the food and beverage services being the primary drivers of expansion.

However, owing to festive demand, the outlook for both Manufacturing and Services activities remain positive over the next quarter.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..