The ASPI surged past the 23,100 mark at the opening bell and sustained that level throughout the session, with mild volatility observed around mid-day.

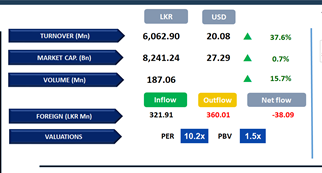

The index ultimately closed at 23,112, recording a gain of 159 points, ahead of the upcoming national budget. Despite the overall positive movement, the number of negative contributors outweighed positive ones.

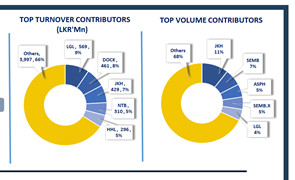

Retail participation remained strong, while HNW activity was moderate. Key positive contributors to the index included SFCL, NDB, DOCK, JKH, and CTHR.

Market turnover stood at LKR 6.1Bn, reflecting an 18% decline from the monthly average of LKR 7.4Bn. The Capital Goods sector led activity, contributing 28% to total turnover, followed by the Banking and Food, Beverage & Tobacco sectors, which jointly accounted for 28%. Meanwhile, foreign investors remained net sellers, posting a net outflow of LKR 38.1Mn for the day.

BOND MARKET

Moderate trading and steady buying in the secondary bond market

The secondary market yield curve experienced moderate trading volumes and activity, supported by continued buying interest today.

In the short end, the 15.02.2028 and 01.07.2028 maturities traded at yields of 9.00% and 9.10%, respectively. The 2029 segment was relatively active as well, with the 15.06.2029, 15.09.2029, 15.10.2029, and 15.12.2029 bonds changing hands within a yield range of 9.48%-9.55%.

In the 2030 maturities, the 15.05.2030 and 01.07.2030 bonds traded between 9.66% and 9.72%. Meanwhile, the longer-dated 01.11.2033 bond recorded trades between 10.55% and 10.58%.

On the external front, the LKR depreciated against the USD, closing at LKR 304.6/USD compared to LKR 304.5/USD seen previously. Overnight liquidity in the banking system contracted to LKR 125.9Bn from LKR 133.2Bn recorded on the previous day.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..