Following the latest decision by the CBSL to increase the overnight policy rate by 100bps at the monetary policy review, coupled with heightened tensions in the Middle East following the US strike on Iranian missile facilities, market sentiment remained negative as both indices closed in negative territory during today’s session.

The ASPI declined by 190 points to close at 22,175, while the S&P SL20 fell by 61 points to settle at 6,118. SAMP, HAYL, JKH, HNB and NDB were among the top negative contributors to the ASPI.

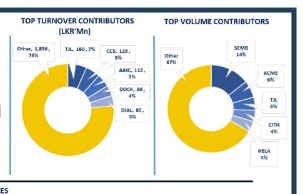

Notable HNW participation was observed, with crossings accounting for 66.4% of total turnover, of which LKR 3.0Bn amounted from a crossing in AAIC, although retail investor participation remained relatively subdued.

Daily turnover stood at LKR 4.9Bn, marking an increase of 46.0% over the monthly average of LKR 3.4Bn. Insurance sector led the daily turnover with a share of 65%, followed by the Banking, and Diversified Financials sectors collectively contributing 15%. AAIC dominated the overall turnover with LKR 3.1Bn (63.5%). Foreign investors remained net sellers, posting a net outflow of LKR 3.0Bn.

BOND MARKET

100bps policy rate hike lifts yields across the curve

The Monetary Policy Board of the Central Bank of Sri Lanka, at its meeting held on 25th May 2026, decided to increase the Overnight Policy Rate (OPR) by 100bps to 8.75% from 7.75%, following a careful assessment of evolving domestic and global economic conditions and the overall outlook.

Following the monetary policy announcement, the secondary market entered a standstill, with trading activity across maturities remaining muted. However, the secondary market yield curve shifted upward, adjusting in line with the rate hike.

Meanwhile, the PDMO raised LKR 95.6Bn at today’s T-Bill auction, below the initially offered amount of LKR 140.0Bn, despite receiving total bids worth LKR 172.3Bn. The PDMO accepted bids exceeding the offered amount for the 3M maturity, raising LKR 71.2Bn, while accepting lower amounts for the 6M and 12M maturities at LKR 14.4Bn and LKR 9.9Bn, respectively.

Weighted average yields increased in line with today’s OPR hike, with the 3M T-Bill yield rising by 118bps to 9.36%, the 6M T-Bill yield increasing by 143bps to 9.68%, and the 12M T-Bill yield climbing by 134bps to 9.83%. Overnight liquidity in the banking system expanded to LKR 142.31Bn from LKR 136.98Bn recorded previously.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..