Amid ongoing unresolved tensions between the US and Iran, coupled with a cautious stance adopted by investors, the Colombo Bourse remained largely stagnant throughout the trading session.

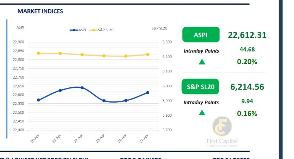

The ASPI recorded a marginal gain of 45 points to close at 22,612, reflecting subdued movement during the day, while the S&P SL20 edged up by 10 points to settle at 6,215.

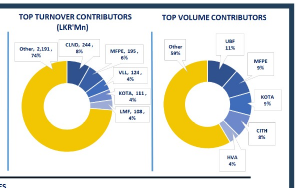

Positive contributions to the ASPI were primarily driven by CINS, DIAL, SAMP, CARS and DFCC. Market participation from both HNW and retail investors remained at moderate levels, with overall sentiment slightly positive yet subdued.

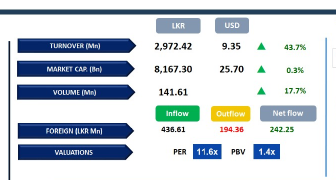

Daily turnover stood at LKR 3.0Bn, marking a decrease of 19.5% over the monthly average of LKR 3.7Bn. Food Beverage & Tobacco sector led the daily turnover with a share of 25%, followed by the Capital Goods, and Real Estate Management & Development sectors collectively contributing 25%. Foreign investors turned net buyers, posting a net inflow of LKR 242.2Mn.

BOND MARKET

Secondary bond market stalls amid geopolitical jitters

The secondary market commenced the week on a subdued note, with activity largely at a standstill, leaving the yield curve broadly unchanged.

Heightened tensions in the Middle East, alongside negative developments surrounding peace talks, continued to fuel uncertainty, driving global oil prices higher.

Against this backdrop, investor participation remained muted, with only minimal and largely insignificant trades observed in the secondary market.

On the external front, the LKR depreciated against the USD, standing at LKR 317.75/USD, compared to LKR 317.17/USD seen yesterday. Liquidity in the banking system expanded to LKR 219.28Bn from LKR 199.17Bn recorded previously.

-First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..