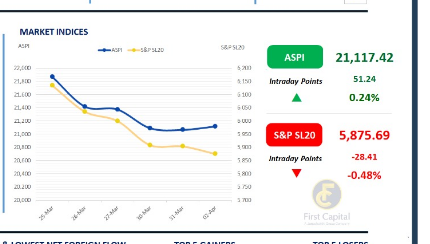

The market ended on a positive note today, with the ASPI gaining 51 points to close at 21,117, while the S&P SL20 index moved in the opposite direction, declining by 28 points to settle at 5,876, primarily weighed down by ex–dividend adjustments in major banking counters.

MELS, CARG, SAMP, CTHR, and RIL emerged as the key drivers behind the ASPI’s upward movement. Market participation was observed at a lower level. Market breadth remained positive, with 138 gainers outpacing 83 decliners.

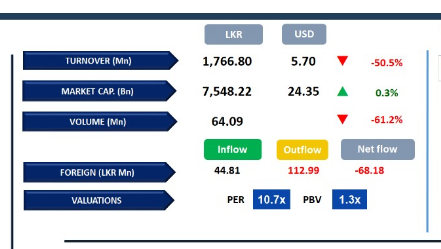

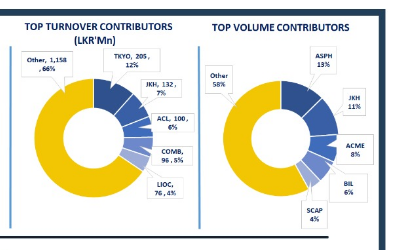

Daily turnover stood at LKR 1.8Bn, marking a decrease of 62.5% over the monthly average of LKR 4.7Bn. Capital Goods sector led the daily turnover with a share of 26%, followed by the Banking and Materials sectors collectively contributing 33%. Foreign investors remained net sellers, posting a net outflow of LKR 68.2Mn.

BOND MARKET

Moderate volumes keep yield curve stable

On the final day of the shortened trading week, the secondary market recorded moderate volumes and activity, with the overall yield curve remaining stable. In the 2029 tenor, the 15.06.2029 and 15.09.2029 maturities traded at 9.90% and 9.95%, respectively. Further along the curve, the 15.03.2030 maturity traded at 10.05%, while the 01.06.2033 maturity traded at 11.05%.

Meanwhile, the 15.06.2034 maturity was observed trading at 11.10%. On the external front, the LKR depreciated against the USD, closing at LKR 315.21/USD compared to LKR 315.19/USD recorded previously. Liquidity in the banking system contracted to LKR 247.36Bn from LKR 322.95Bn recorded previously.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..