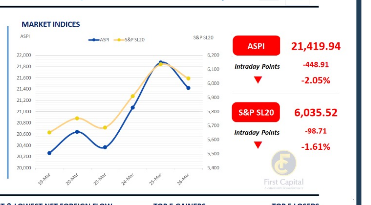

Amid heightened uncertainty surrounding US–Iran peace negotiations, coupled with profit-taking activity, the Colombo bourse closed on a weaker note today.

The ASPI declined by 449 points to settle at 21,420, while the S&P SL20 fell by 99 points to close at 6,036. HNB, MELS, COMB, CTHR and JKH emerged as the top negative contributors to the ASPI. Participation from both HNW and retail investors remained at average levels.

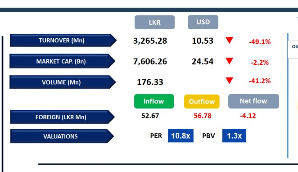

Daily turnover stood at LKR 3.3Bn, reflecting a decline of 36.6% compared to the monthly average of LKR 5.2Bn, with crossings accounting for 13.2% of total turnover.

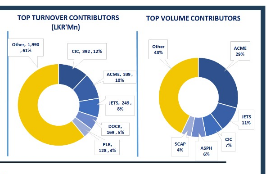

The Materials sector led the daily turnover with a 25% share, followed by the Capital Goods and Banking sectors, which together contributed 27%. Foreign investors continued to be net sellers, recording a net outflow of LKR 4.1Mn

BOND MARKET

Selling pressure rises as geopolitical tensions weigh on sentiment

Amidst a re-escalation of tensions in the Middle East, secondary market investors once again adopted a selling stance, despite subdued activity levels, resulting in only moderate volumes.

At the short end, activity was observed in the 2028 segment, with maturities dated 15.02.2028, 15.03.2028, 01.05.2028 and 15.12.2028, trading from 9.55% to 9.75%.

Furthermore, 15.06.2029, 15.10.2029 and 15.12.2029 maturities traded between 9.80% to 9.90%. Approaching the belly end, 01.03.2030 and 15.10.2030 bonds were seen trading from 10.00% to 10.10%, whilst the 15.03.2031 maturity changed hands between 10.05% to 10.10%.

Lastly, within the 2033 segment, bonds bearing maturities of 01.06.2033 and 01.11.2033 traded between 10.90% to 11.00%. On the external front, the LKR appreciated against the USD, closing at LKR 313.51/USD compared to LKR 314.22/USD recorded previously. Liquidity in the banking system contracted to LKR 292.29Bn from LKR 298.34Bn recorded previously.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..