Colombo Bourse recorded a moderate gain during the session, supported by improved domestic trading momentum and ease in global oil prices, despite escalating geopolitical tensions in the Middle East.

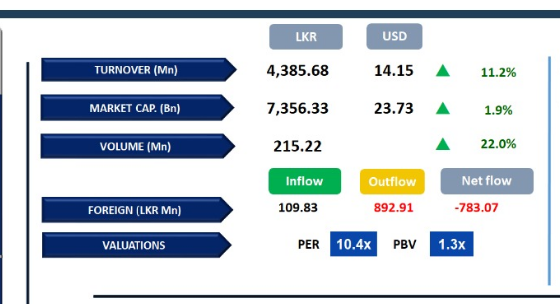

Investors actively engaged in bargain hunting, particularly within banking sector counters, driving market activity. ASPI advanced by 376 points to close at 20,640, while the S&P SL20 Index gained 101 points to settle at 5,752. SAMP, HAYL, JKH, DOCK and MELS emerged as the top positive contributors to the index.

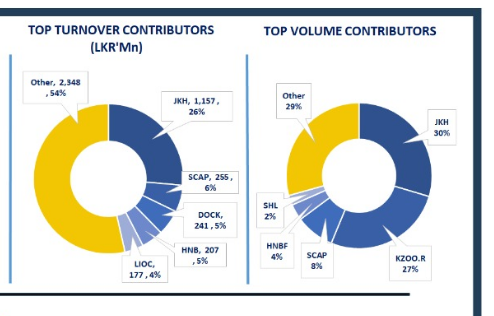

Retail participation remained relatively subdued, whereas HNW investor activity was elevated, with notable interest in JKH, which recorded LKR 628.0Mn in crossings, followed by HNB and DOCK. Market turnover recorded at LKR 4.4Bn, representing a 12.9% decline over the monthly average of LKR 5.0Bn.

Capital Goods sector led the daily turnover with a share of 42%, followed by the Banking, and Insurance sectors collectively contributing 25%. Foreign investors remained net sellers, posting a net outflow of LKR 783.1Mn.

BOND MARKET

Yields ease marginally amid moderate market activity

The secondary market saw moderate trading activity with steady volumes, while the overall yield curve softened slightly. Among the maturities traded, the 15.09.2029 bond was seen at 9.75%, while the 15.12.2029 traded at 9.80% and the 01.03.2030 at 10.00%.

Further along the curve, the 15.03.2031 maturity moved within a narrow band of 10.00%-10.10%. In the 2033 segment, both the 01.06.2033 and 01.11.2033 maturities traded in the range of 11.00%-10.92%. Toward the longer end, the 15.06.2034 maturity was observed between 11.05%–11.00%, while the 15.06.2035 traded at 11.05%.

On the external front, the LKR depreciated marginally against the USD, closing at LKR 311.4/USD compared to LKR 311.3/USD recorded previously. Liquidity in the banking system contracted to LKR 323.0Bn from LKR 351.0Bn recorded previously.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..