The Colombo Bourse experienced some morning volatility and a mild midday dip, while both indices recovered in the afternoon, suggesting selective buying interest rather than broad-based momentum.

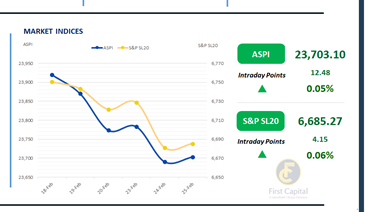

ASPI edged up by 12 points to settle at 23,703 and S&P SL20 gained 4 points to close at 6,685. CDB, DIAL, PLR, JKH, and DOCK emerged as the key positive contributors to the index. Market breadth was negative, with 127 counters declining and weighing on the index, compared to 101 counters that posted gains, indicating that the day’s advance was driven by a select group of stocks, despite the overall positive close.

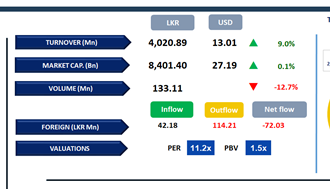

Retail investors were the primary participants during today’s session, while HNW activity appeared modest. Daily turnover stood at LKR 4.0Bn, marking a decrease of 34.5% over the monthly average of LKR 6.1Bn.

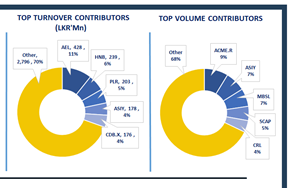

Diversified Financials sector led the daily turnover with a share of 22%, followed by the Capital Goods, and Banking sectors collectively contributing 35%. Foreign investors remained net sellers, posting a net outflow of LKR 72.0Mn bringing the year-to-date foreign outflow to LKR 15.9Bn.

BOND MARKET

T-Bill auction yields decline across the board

Ahead of tomorrow’s T-Bond auction, the secondary market witnessed slight buying interest amid limited activity and thin trading volumes. Within the 2028 maturities, 15.02.2028, 01.05.2028, and 15.10.2028 traded in the range of 8.98% to 9.12%.

Further along the yield curve, 15.09.2029, 15.10.2029 and 15.12.2029 traded between 9.45% and 9.48%. The 01.03.2030 maturity changed hands at 9.55%, while 15.06.2035 was traded at 10.80%. The Public Debt Management Office completed its weekly T-Bill auction, securing LKR 67.9Bn while accepting only a portion of the total amount offered.

The weighted average yields inched down across all tenures with that of the 3M Bill inching down by 3bps to settle at 7.63% while that of the 6M and 12M tenures dipped by 7bps and 3bps, settling at 7.92% and 8.24% respectively.

On the external front, the LKR slightly appreciated against the USD, closing at LKR 309.37/USD compared to LKR 309.38/USD recorded the previous day. Overnight liquidity in the banking system expanded to LKR 322.93Bn from LKR 297.94Bn recorded previously.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..