The ASPI initially surpassed the 22,800 mark during early trading; however, heightened selling pressure dragged the index below 22,600 by midday.

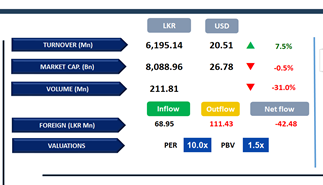

Despite this, selling momentum eased during the latter half of the session, allowing the market to recover partially and close at 22,689, reflecting a decline of 100 points compared to the previous session.

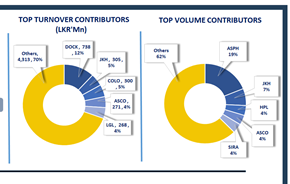

Retail participation remained robust, with notable interest in DOCK, while HNW activity was comparatively moderate. Key negative contributors to the index included JKH, SFCL, SAMP, CTHR, and LOLC.

Market turnover amounted to LKR 6.2Bn, approximately 17% below the monthly average of LKR 7.4Bn. The Capital Goods sector led market activity, accounting for 33% of total turnover, followed by the Food, Beverage, and Banking sectors, which jointly contributed 21%.

Meanwhile, foreign investors turned net sellers, recording a net outflow of LKR 42.5Mn for the day.

BOND MARKET

Belly end yields ease slightly

The secondary market yield curve reflected mixed sentiment, with moderate trading volumes and diverse activity across maturities.

Yields edged lower, particularly at the belly end of the curve. At the short end of the curve, the 15.01.2028 and 15.03.2028 maturities traded at 9.17%.

Meanwhile, other 2028 maturities, 01.05.2028, 01.07.2028, and 15.10.2028, traded at the rates of 9.20%, 9.25%, and 9.26%, respectively. Further along the curve, the 15.10.2029, 15.05.2030, 01.07.2030, 15.03.2031, and 01.07.2032 maturities changed hands at the rates of 9.68%, 9.74%, 9.77%, 10.15%, and 10.75%, respectively.

On the external front, the LKR depreciated against the USD, closing at LKR 304.0/USD compared to LKR 303.8/USD seen previously. Overnight liquidity in the banking system expanded to LKR 144.3Bn from LKR 135.1Bn recorded the previous day.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..