Echoing the selling sentiment from the previous week, the CSE experienced continued profit-taking, with selling pressure concentrated in Banking and blue-chip counters weighing down the index.

The ASPI opened the day under selling pressure, followed by a phase of bargain hunting. Despite this, the index failed to recover and ended the day in negative territory.

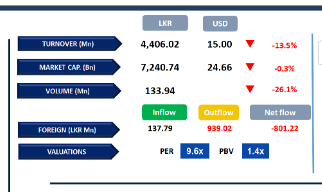

Accordingly, the ASPI ended the session at 20,576, recording a loss of 74 points. Key negative contributors to the index included HNB, JKH, COMB, HAYL, and CARG.

Investor participation remained relatively subdued, with limited activity from both retail and HNW investors. As a result, market turnover dropped to LKR 4.4Bn, marking over a one-week low and reflecting a 31% decline compared to the monthly average of LKR 6.4Bn.

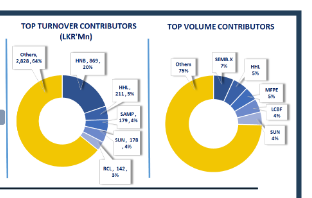

The Banking sector led turnover contributions, accounting for 31% of the total, while the Capital Goods and Diversified Financials sectors together made up 35% of the overall turnover. Foreign investors remained net sellers with a net outflow of LKR 801.2Mn.

A lacklustre mood marks the week's start

The secondary market stepped into the trading week with restrained dynamism as investor activity appeared muted prompting a static yield curve.

While noteworthy activity was scarce, the short end of the curve registered a few trades, with 15.01.2027 trading at 8.20% while 01.05.2027 and 15.09.2027 traded at 8.44% and 8.60% respectively.

Moving ahead, 01.05.2028 was seen changing hands at 8.85%. Finally, the 15.12.2032 maturity traded between the narrow range of 10.28% to 10.30%.

In the forex market, the LKR depreciated against the greenback, closing at LKR 302.0/USD compared to LKR 301.8/USD seen previously. Meanwhile, overnight liquidity in the banking system contracted to LKR 111.6Bn from the previously seen level of LKR 116.4Bn.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..