The Broad Market experienced another day of bullish momentum, driven by rising investor optimism, leading to a decline in risk premiums, and heightened participation from both retail and HNW investors.

The recently released 3Q2024 results of PABC and SEYB have bolstered positive sentiment towards the Banking sector, as investors continue to maintain their bullish outlook on Banking sector stocks.

Accordingly, the ASPI closed the day at 12,771 gaining 25 points with MELS, NDB, CFIN, HAYL and TKYO emerging as the top positive contributors to the index.

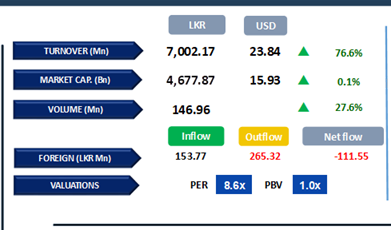

Meanwhile, amidst multiple crossings, turnover experienced a 76.6% increase from yesterday and stood at LKR 7.0Bn, marking over a 100% increase monthly average standing at LKR 2.5Bn.

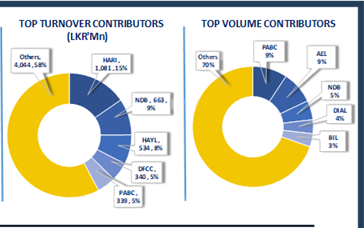

Out of 15 off-board transactions, notable trades were recorded in HARI and SWAD, trading 13.9% and 10.7% stakes at LKR 4,040.5/share and LKR 15,003.5/share respectively.

The Banking sector led turnover by 34%, followed by the Food, Beverage & Tobacco and Capital Goods sectors jointly contributing 39% of the overall turnover. Foreign investors turned net sellers, with a net outflow of LKR 111.5Mn.

Secondary market on a dismal stance

The secondary bond market witnessed very thin trading volumes and low investor activity during the day continuing from the previous session.

Maturities across the board remained broadly unchanged as investors longed for clear market sentiment. Amongst the limited maturities traded liquid maturities namely, 15.09.27 maturity traded at 11.50%, 01.05.28 tenor traded at 11.80%, 15.12.28 maturity traded at 11.90%.

On the long end of the curve 15.10.30 maturity traded at 12.24%. Notably CCPI inflation for Oct 2024 recorded in the negative territory for the second consecutive time registering at -0.8% on a YoY basis compared to -0.5% recorded during the month of Sep 2024.

Overnight liquidity increased during the day recording at LKR 179.5Bn compared to LKR 126.9Bn recorded during the previous day moreover, CBSL holdings remained unchanged at LKR 2,515.6Bn. On the externals side LKR slightly depreciated against the USD recording at LKR 293.7 compared to LKR 293.5 recorded during the previous day.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..