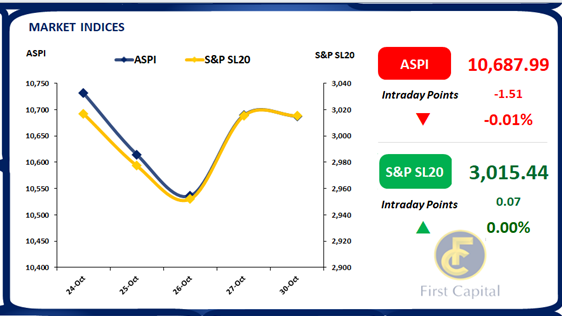

The market adopted a cautious stance, with investors adopting a wait and see approach in anticipation of the upcoming budget. Consequently, the ASPI maintained a relatively flat trajectory, closing just marginally in the red at 10,688, with a minor decline of only 2 points.

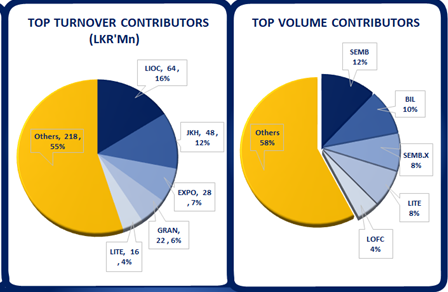

Amongst the top turnovers for the day, LIOC stood out, as it reported over 100% QoQ growth in earnings for the latest quarter. However, EXPO observed selling interest due to unfavorable results whilst retail investors remained active amidst relatively thin volumes.

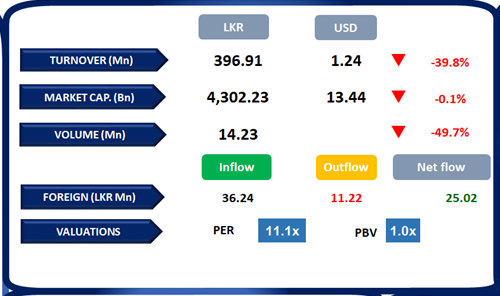

In the backdrop of this, foreign buying interest persisted for the fifth consecutive day, and JKH continued to attract the highest foreign inflow, amounting to LKR 30.9Mn. Meanwhile, the market turnover marked a 5-month low, recording LKR 397.0Mn, which is a 58% decrease compared to the monthly average turnover of LKR 945.2Mn. Notably, the Capital Goods, Food, Beverage, Tobacco, and Energy sectors collectively accounted for 54% of the overall turnover.

Bond auction fully rejected; short to mid active in the secondary market

CBSL conducted its second bond auction for the month of October expecting to raise LKR 45.0Bn. However, CBSL fully rejected bids for both 15.03.2028 and 15.03.2031. Meanwhile, in the secondary market, activities took a mixed sentiment prior and after the bond auction, with interest largely centered across short to mid tenors.

Accordingly, 2025 maturities 15.01.2025, 01.06.2025 and 01.07.2025 traded in the range of 14.90%-15.15%. Meanwhile, on the mid end 15.05.2026, 01.06.2026, 01.08.2026 and 15.09.2027 hovered between 14.95%-15.05%. Activities were also enticed on the long end where 15.05.2030 recorded trades at 14.25%. On the external side LKR continued to depreciate against the USD and closed at LKR 327.1.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..