The Colombo Bourse recorded a subdued trading session today, reflecting weakened investor confidence. Although the market experienced a brief upward movement at the commencement of trading, the momentum reversed, resulting in largely stagnant market activity for the remainder of the session.

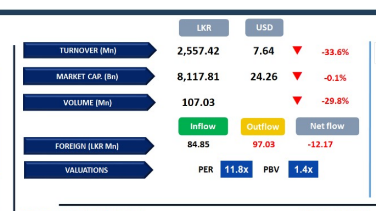

The ASPI edged up by 9 points to close at 22,386, while the S&P SL20 declined by 11 points to settle at 6,211. CTHR, LION, HAYL, SPEN, and SDB were the leading positive contributors to the ASPI.

Participation from both HNW and retail investors remained relatively muted, amid a mixed market sentiment. Daily turnover stood at LKR 2.6Bn, marking a decrease of 12.4% over the monthly average of LKR 2.9Bn.

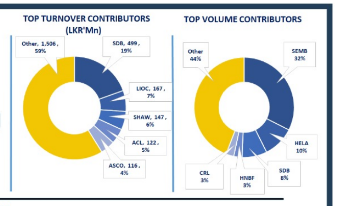

Banking sector led the daily turnover with a share of 29%, followed by the Capital Goods, and Real Estate Management & Development sectors collectively contributing 26%. Foreign investors turned net sellers, posting a net outflow of LKR 12.2Mn.

BOND MARKET

Secondary market activity surges on pre-auction buying interest

The secondary market extended the positive sentiment observed in previous sessions, with investors maintaining strong buying interest ahead of today’s T-Bill auction, resulting in a broad-based easing of yields.

Following the auction, mild selling interest emerged, however, market activity and trading volumes remained elevated throughout the session, reflecting sustained investor participation.

At the short end of the curve, the 01.05.2027 and 15.09.2027 maturities traded from 10.55% to 10.35%. Moving on to the 2028 segment, the 15.02.2028 maturity traded at 10.55%, followed by the 01.05.2028, 01.07.2028 and 15.10.2028 maturities, all trading from 10.75% to 10.65%.

The 15.12.2029 bond changed hands from 11.10% to 11.00%, and within the 2030 segment, the 01.03.2030, 15.05.2030 and 01.08.2030 maturities traded from 11.50% to 11.05%.

Moving further along the belly end, the 01.12.2031 maturity traded at 11.75%, the 15.12.2032 maturity traded from 11.60% to 11.45% and within the 2033 segment, maturities dated 15.01.2033 and 01.06.2033 traded from 11.65% to 11.50%.

The 15.06.2034 bond traded at 11.80%, followed by the 15.03.2035 bond from 12.00% to 11.77% and lastly, the 15.08.2036 bond traded at 11.90%. The PDMO successfully raised the full offered amount of LKR 70.0Bn, attracting total bids of LKR 129.4Bn. Of the amount raised, LKR 51.6Bn was accepted in the 3-month tenor, LKR 8.7Bn in the 6-month tenor, and LKR 9.6Bn in the 12-month tenor.

The weighted average yield on the 3-month bill declined by 7bps to 10.02%, while the 6-month bill yield fell by 11bps to 10.16%, whilst the 12-month bill yield remained unchanged at 10.16%.

On the external front, the LKR depreciated against the USD, standing at LKR 334.58/USD, compared to LKR 331.59/USD seen earlier. Liquidity in the banking system expanded marginally to LKR 43.19Bn from LKR 40.07Bn recorded previously.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..