The Colombo Bourse trended positively throughout the session, with both indices maintaining upward momentum after a steady start.

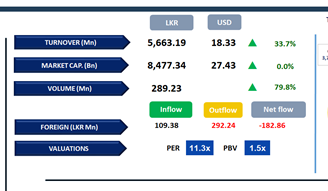

Gains strengthened in the latter half of the day. ASPI advanced by 37 points to close at 23,920, while the S&P SL20 index recorded a gain of 42 points to settle at 6,751. Leading positive contributors to the ASPI were SAMP, HNB, JKH, ACL and DIAL.

Market breadth was positive, with 105 advancing counters outpacing 124 decliners backed by the gain in banking and blue-chip counters. HNW investor participation remained subdued, while retail investor activity was high, particularly in retail trading stocks.

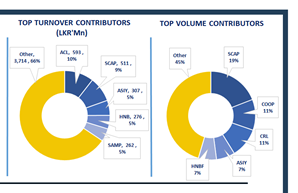

Daily turnover stood at LKR 5.7Bn, marking a decrease of 15.3% over the monthly average of LKR 6.7Bn. Capital Goods sector led the daily turnover with a share of 25%, followed by Diversified Financials, and Banking sectors collectively contributing 34%.

Foreign investors remained net sellers for the 22nd consecutive session, recording a net outflow of LKR 182.9Mn for the day, bringing the cumulative net foreign outflow to LKR 11.8Bn.

BOND MARKET

T-Bill auction yields decline across the board

The secondary market yield curve remained largely unchanged, with moderate trading volumes and mixed activity. Within the 2028 maturities, 15.02.2028, 15.03.2028, 01.07.2028, and 01.09.2028 traded in the range of 8.90% to 9.15%.

Further along the yield curve, 15.05.2029, 01.06.2029, 15.09.2029, and 15.12.2029 traded between 9.34% and 9.50%. The 01.03.2030 maturity changed hands at 9.55%, while 01.07.2030 and 15.10.2030 were traded at 9.58%.

At the longer end of the curve, 15.03.2031, 15.12.2032, 15.06.2032, and 01.07.2037 traded at 9.75%, 10.15%, 10.75%, and 10.87%, respectively. Public Debt Management Office concluded its weekly T-Bill auction where LKR 60.0Bn was raised, accepting the fully offered amount.

The weighted average yields inched down across all tenures with that of the 3M Bill inching down by 6bps to settle at 7.66% while that of the 6M and 12M tenures dipped by 8bps and 4bps, settling at 7.99% and 8.27% respectively.

On the external front, the LKR slightly depreciated against the USD, closing at LKR 309.32/USD compared to LKR 309.22/USD recorded the previous day. Overnight liquidity in the banking system expanded to LKR 282.43Bn from LKR 270.41Bn recorded previously.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..