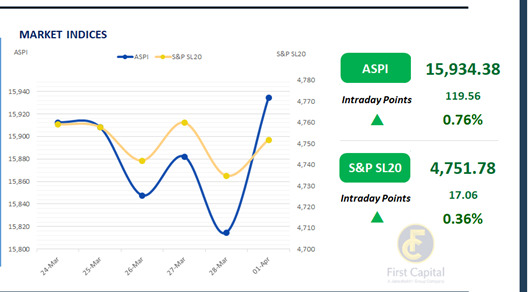

The first trading session for April commenced on a negative note for a short while, with the ASPI dropping as the market opened.

This trend soon reversed as it began picking up and building on positive momentum throughout the rest of the day. The ASPI closed in the green gaining 120 points, reflecting a 0.76% gain to close at 15,934.

The initial drop in the index was largely fueled by the banking sector as most banks’ XD date being today led to added selling pressure among certain investors.

Retail investors demonstrated increased participation while HNW investors had a quiet trading session with only one crossing present.

There was mixed sentiment towards banking counters while positive sentiment was noted towards blue-chip stocks. MELS, HAYL, HNB, NDB and LOLC emerged as the top positive contributors to the index, while SAMP, COMB, CINS, CARS and ASPH were the top negative contributors.

The turnover stood at LKR 1.9Bn, marking a 9.1% decrease from the monthly average of LKR 2.1Bn. The Banking sector was the most significant contributor to the overall turnover with a 29% share, followed by the Capital Goods sector at 23% and the Diversified Financials Sector at 12%. Foreign investors were net sellers, with a net outflow of LKR 75.4Mn.

April opens bond market with mild buying sentiment

April commenced with modest buying sentiment in the secondary bond market, accompanied by moderate trading volumes. On the shorter end of the yield curve, the 01.02.2026 and 01.08.2026 bonds were traded within a range of 8.30% to 8.65%.

Moving further along, the 01.05.2027, 15.09.2027, and 15.10.2027 maturities saw trades between 9.30% and 9.50%. Additionally, the 15.02.2028, 15.03.2028, and 01.05.2028 bonds transacted within the 9.93% to 10.03% range, while the 01.07.2028 and 15.12.2028 issues were traded between 10.05% and 10.15%.

Lastly, the 15.06.2029 maturity saw trading between 10.25% and 10.35%. In the forex market, the LKR showcased a marginal appreciation against the greenback, standing at LKR 296.32/USD in comparison to 296.35/USD registered on the previous day.

Meanwhile, overnight liquidity in the banking system contracted to LKR 171.9Bn from LKR 184.6Bn on the previous session.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..