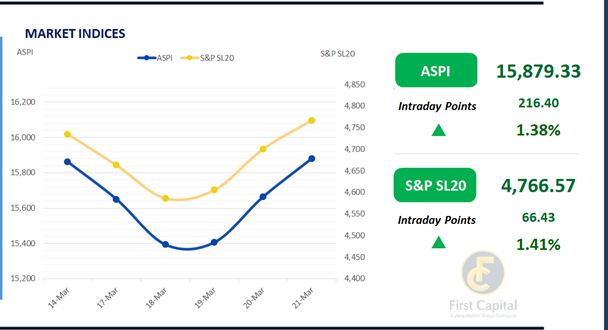

The market remained gripped by yesterday’s bullish turn, fueling a further rally in the ASPI. The ASPI climbed, retaining a consistent upward momentum through the day, amid feeble volatility.

Consequently, the index ended the day in the green at 15,879, having registered a staggering gain of 216 points which in turn translated to an uptick of 1.4%.

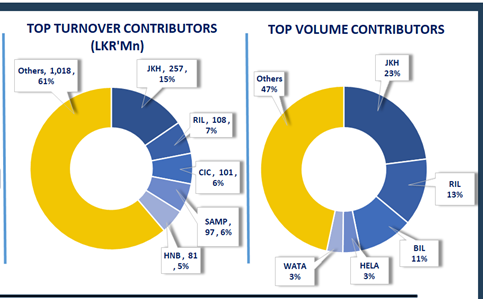

The Banking sector once again stood out as a salient driver of ASPI’s performance with COMB, HNB, NDB and DFCC emerging as the top positive contributors followed by CARS.

Today’s gains were mostly a result of the conspicuous buying sentiment that overtook the market, particularly from HNW investors.

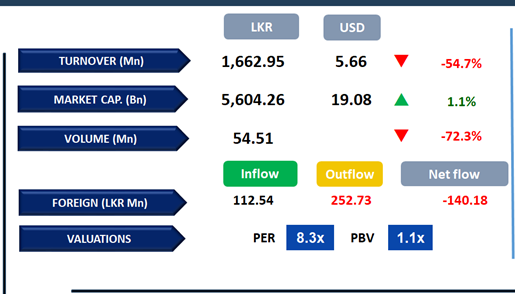

Turnover dipped to LKR 1.7Bn from yesterday’s LKR 3.7Bn level, falling behind the monthly average of LKR 2.3Bn. The Capital Goods sector dominated contributions to turnover with a share of 32%

.

.

This was followed by the Banking sector and the Food, Beverage and Tobacco sector which produced a joint contribution of 32%. Foreign investors were net sellers, accounting for a net outflow of LKR 140.2Mn, amid subdued participation.

Yield curve continues to decline as the week ends

The secondary market closed the week with continued buying interest from previous days, resulting in high trading volumes and activity.

Amongst the traded maturities, at the short end, 2026 and 2027 maturities were traded within a range of 10.05% to 9.40%. 2028 maturities, the 15.02.2028, 15.03.2028, and 01.05.2028 bonds were traded between 9.65% and 9.55%, while the 01.07.2028, 01.09.2028, 15.10.2028, and 15.12.2028 bonds saw trades within the range of 9.90% to 9.75%.

Additionally, the 15.06.2029 and 15.09.2029 bonds were traded between 10.05% and 10.00%. Furthermore, the 15.12.3032 bond traded within the range of 10.60% and 10.50%, and towards the long end, 01.06.2033 bond traded between 10.85% to 10.65%.

On the external front, the LKR depreciated against the USD, closing at LKR 296.0/USD in comparison to LKR 296.20/USD registered on the previous day. CBSL holdings of government securities remained stagnant at LKR 2,511.9Bn. Overnight liquidity of the Banking system contracted to LKR 156.0Bn from LKR 179.0Bn recorded yesterday.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..