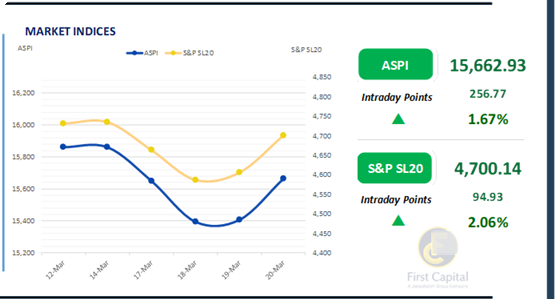

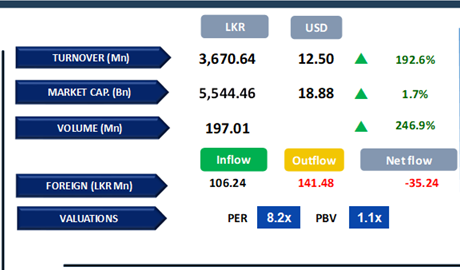

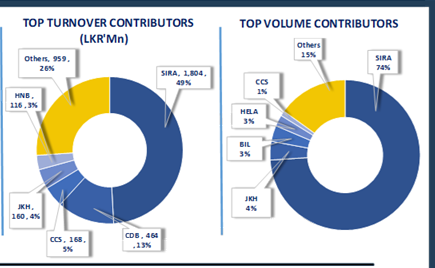

The market saw a bullish momentum today reversing some of the lost ground as the ASPI gained 257 points to close at 15,663. Turnover reached LKR 3.7Bn, with over 50% of turnover dominated by SIRA consisting of a large volume of 146.0Mn shares.

The positive contributors for the day were COMB, HNB, JKH, SAMP and DFCC. Despite the overall market gains, retail participation remained low compared to yesterday, with the majority of turnover driven by HNW investors.

The Banking sector was the primary driver behind the market’s positive movement today. Yesterday's positive buying sentiment continued into today, supporting the overall market uptick.

The market showed resilience, with strong contributions from Banking stocks, while retail activity remained subdued. Capital Goods sector was the most significant contributor to the overall turnover with a 58% share, followed by the Diversified Financials, and the Banking sectors jointly accounting for 25%. Foreign investors turned into net sellers, with a net outflow of LKR 35.2Mn.

Buying interest persists despite signs of mixed sentiment

The buying sentiment that prevailed over the last few days continued to persist amid some mixed sentiment that was particularly evident for 2028 and 2029 maturities.

However, market participants continued to demonstrate buying interest for 2030, 2031 and 2032 maturities. At the mid end of the secondary market’s yield curve, the 15.02.2028 and 15.03.2028 traded within the range of 9.65% - 9.72%.

Meanwhile, 01.05.2028, 01.07.2028, 15.10.2028 and 15.12.2028 traded at a marginally higher range of 9.75% - 9.90%. Moving ahead of the yield curve, the 15.09.2029 and 15.12.2029 maturities traded at 10.03% - 10.15% while 15.05.2030 and 15.10.2030 maturities traded within the range of 10.25% - 10.16%.

Moreover, the 15.03.2030 maturity traded at 10.65% - 10.50%. Finally, the 01.07.2032, 01.10.2032 and 15.12.2032 maturities traded between 10.90% to 10.65% while the 01.06.2033 maturity traded at 11.00%.

On the external front, the LKR depreciated against the USD, closing at LKR 296.2/USD in comparison to LKR 296.0/USD registered on the previous day. CBSL holdings of government securities remained stagnant at LKR 2,511.9Bn. Overnight liquidity of the Banking system expanded to LKR 178.9Bn from LKR 172.1Bn recorded yesterday.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..